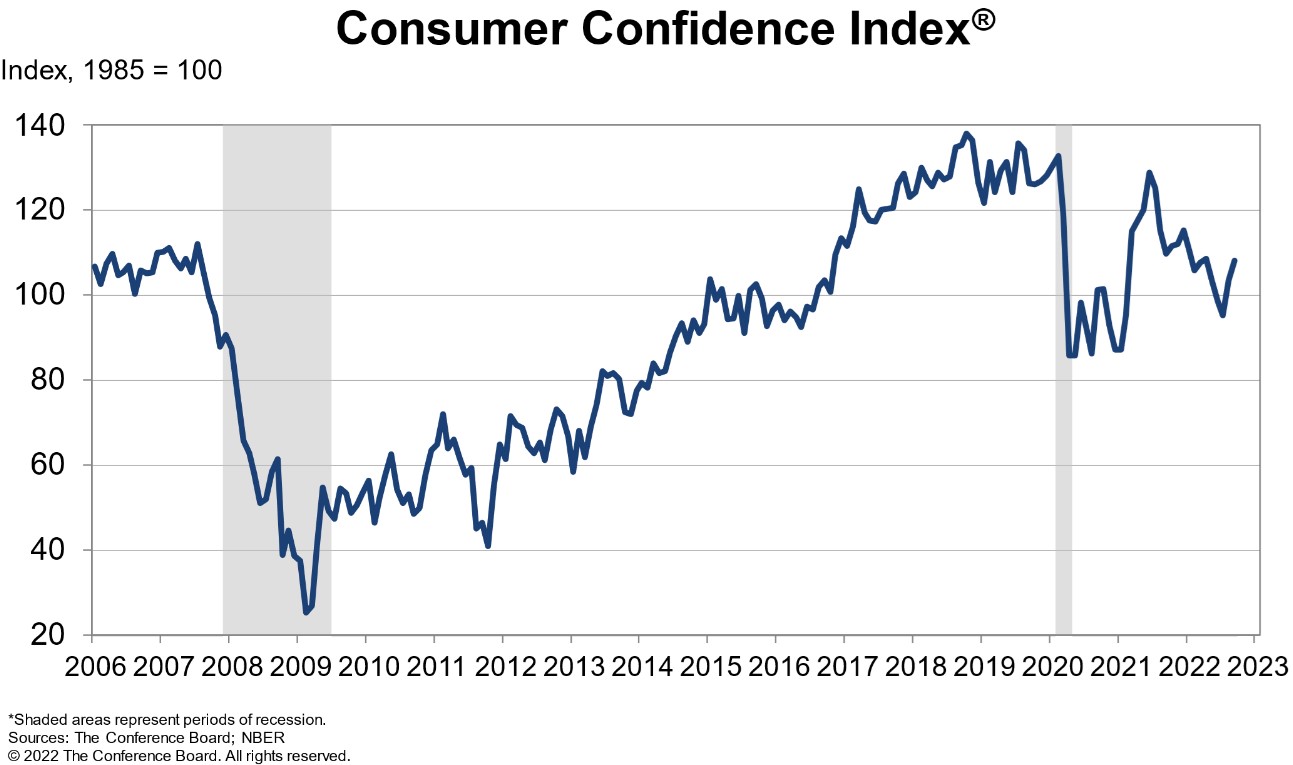

The Conference Board Consumer Confidence Index® increased in September for the second consecutive month. The Index now stands at 108.0 (1985=100), up from 103.6 in August. “Consumer confidence improved in September for the second consecutive month supported in particular by jobs, wages, and declining gas prices,” said Lynn Franco, Senior Director of Economic Indicators at The Conference Board.

Although consumer confidence and positive thinking will serve you well, don’t stop yourself from preparing for unexpected catastrophes such as job loss, serious illness, death, or divorce. As ugly as that sounds, it’s unwise to procrastinate or avoid making plans to get you through tough times. Here are some tough questions to ask yourself when developing a contingency plan:

- How long can I pay my existing bills if I lose my paycheck? What expenses could I cut?

- How long do I get paid if I am sick and unable to work?

- How long can I keep my group benefits?

- What are my financial obligations if I were to die unexpectedly?

- How much income would my family need to maintain the existing household?

- How long would my assets last if long-term medical care is needed? Would my spouse have adequate income?

Develop a Plan

You need to develop a contingency plan just in case calamity strikes. Your strategy should easily integrate into your day-to-day financial decisions. If you have high mortgage, auto, and credit card debt, you are at greater risk due to loss of income. As you make critical financial decisions, ask yourself whether you can continue to meet your obligations even if you lose your job or experience significant income loss.

Create an Emergency Fund

Establish an emergency fund of approximately six months of living expenses. This fund will provide cash flow for short-term income loss and protect your retirement investments from the penalties and fees of cashing out. An emergency fund will protect you from creating more problems by using your credit card for emergencies.

Evaluate Your Insurance

It’s also important to look at your life and disability insurance options. Are your life insurance benefits adequate? How much of your life insurance is related to your job? You might need a personal policy that provides sufficient coverage for your needs. Do you have insurance that replaces your income if you become sick or hurt? A good disability policy should substitute at least 60% of your income for several years.

Some group plans provide taxable benefits when received, creating an unexpected shortfall in income when needed. You might need to personally supplement your group plan with an individual policy to make up the difference. If you are nearing retirement, you could take out insurance to cover long-term medical care. Even a well-funded retirement account can deplete in a short time if you or your spouse needs this care. Will your existing retirement plan cover care costs and still provide a lifetime income to the healthy spouse?

Update Your Will (or Get One)

Update your estate planning documents, such as wills and trusts, to reflect your wishes. They should also provide instruction for your loved ones in case you become incapacitated and unable to provide guidance. Of course, it isn’t easy to think about worst-case scenarios, but these things happen.

Your Financial Advisor

Nobody is immune to illness, accidents, and adverse events, such as inflation, market volatility, and war. The more you prepare your contingency plan, the better you will weather these storms and emerge with your financial plan intact. For a second opinion, general questions, or guidance, contact our office at (215) 968-1820.